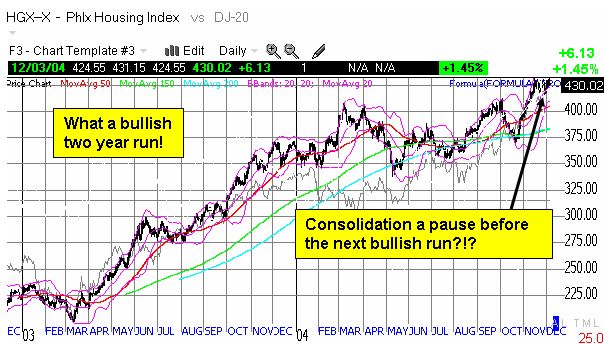

Gold Rush

Down

By Duru

December 5,

2004

I have been

looking for another nice buying opportunity for gold for weeks, and on Thursday

I finally got it. Gold had been dribbling away for two weeks or so ever since

the introduction of the gold ETF - GLD - marked a short-term top in the yellow

metal. A friend and I had been eagerly awaiting GLD ever since the markets

first whispered about it last year. As the debutante's entry to the ball

continued to experience delay after delay, we began to suspect that the coy GLD

would finally come just as the party had hit its peak. Why did gold go down

anyway? Well, the dollar has been on a one-way ticket to Downsville, and it has

become what technicians call extremely oversold. The dollar has not been this

low since 1995-96. A reaction rally in the dollar has been long overdue and

when the dollar finally spiked on Thursday all sorts of speculators and the

like all at once headed for the exits on their hedges against the weakening

dollar - mainly certain gold stocks. It was the classic panic move, and one

that was made without regard to the longer-term fundamentals of continued

record-breaking budget deficits in the

To make the

short-term picture even more manic, the jobs numbers came in anemic once again.

For whatever reason, economists had largely agreed that the

In the middle

of all this drama, oil has been on a

one-month retreat (apparently the Saudis got their instructions mixed up and sent

oil spiraling downward after the

So where does

all this leave us? At the beginning of November, I essentially taunted the bears and claimed that

the market was kicking into a higher gear. Incredibly, I nailed that call

and the bears have been grumbling ever since. As my faithful readers can

imagine, it was a very uncomfortable call for me to make given my persistent

angst over the mounting debt that is helping the economy to limp along. But I

am also not one to argue with the market or to try to talk it down. Overall,

the market continues to look good to me in the short-term. I suspect that any correction

worth talking about is at least another earnings season away. Bushie will get inaugurated

right in the middle of earnings season, and we know how the market likes to

mark big dates with substantial moves before or after these things. Keep an eye

out and as always, be careful out there!