Knocking

Out Craters: FORM, UTSI, EBAY

By Duru

January 6,

2005

This has been

one rough week. While the selling finally let up in the major market indices

today, many stocks, especially tech stocks, continued to suffer heavily.

Here I take a

look at two stocks whose selling portended vicious earnings and revenue

warnings. The implication is that we probably need to take these mini-collapses

very seriously. Greenie and the

Fed fretted in last month's meeting that capital spending on tech was softening.

I think we should heed their warning big-time!

(Click here

for disclaimer that applies to this market analysis)

FORM

FORM is one of

my favorite semiconductor stocks. This stock even made it into my inaugural piece on the madness in the

markets. Well, it looks like the sellers finally got the best of FORM. After

the market closed they warned of a serious shortfall in their expected earnings:

"FormFactor Inc…lowered its outlook for its fiscal fourth quarter ended

Dec. 25, 2004, cutting earnings per share by 6 cents from its previous view of

18 cents to 19 cents per share….preliminary revenue was $46.1 million for the

fourth quarter, lower than the $50 million to $53 million it expected."

Traders and investors responded promptly by cratering the stock almost 17% to

about $19/share. If this level holds it will take FORM back to the lows from

the last earnings report that folks first hated and then loved. Looks like the

first emotion was the correct one!

A collapse

back to $19 puts FORM deep under the 200DMA and into serious selling territory.

Expect any bounce to stall out at the $21 level. I suspect the NASDAQ is going

to have to do some serious repairing before stocks like FORM can begin any kind

of real recovery.

UTSI

UTSI is a

stock I have followed ever since its IPO. I have long been a fan but have been

in fair-weather mode. I missed most of its post-bubble recovery as I had given

up on riding my IRA to stardom with it. However, things in 2004 really spiced

up for UTSI. I wrote

about some of the drama as a guest on Mike's site in mid-October. Back then,

I noted that there was an explosive divergence of opinion between the insiders

who were buying the stock, and all the analysts who had been regularly deriding

UTSI's prospects. For the rest of the year, the insiders were mainly winning

the battle. But reality can be a harsh task master. After hours tonight, these

same insiders had to stand down and admit that they have run into a serious

bump in the business: they cut 4th quarter revenue expectations from

$875-885M to $740-745M. Analysts were expecting 1 cent per share in profits,

but UTSI says now they will lose 40-45 cents. However, they

expect to nab 20-22 cents in profit next quarter on revenue of $770-780M, while

analysts were only expecting 12 cents on $811 in revenue. I am thinking some

profits are getting shifted out. For those of you speculating in

Since I had

been betting alongside the insiders, I got nailed along with the rest of the

faithful. Unfortunately, I allowed the slow and steady rise in the stock lull

me out of a previously hedged position. Interesting to note that the stock sold

off right to the levels ($16 and some change) at which insiders were buying

their shares back in September. Do I daresay this is a buying opportunity if

the stock holds? Yikes!

Also notice

how UTSI never did break resistance at the 200DMA. It barely nicked those

levels on Tuesday. Needless to say this moving average will be a major line to

watch as the stock attempts to recover (again) over the coming months.

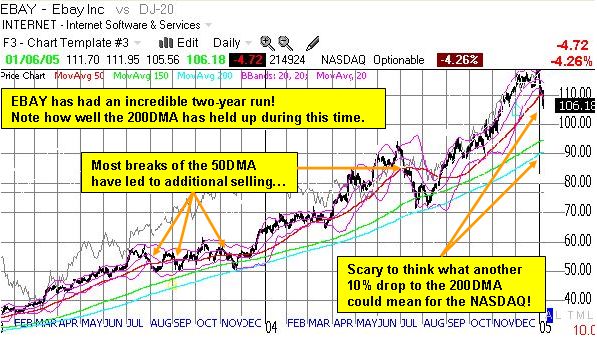

EBAY

It took the

entire week, but finally some of the big-cap, blue chip tech stocks cratered

below their 50DMA. This can be seen as the NASDAQ also finally closed a hair

below this important support level. This is where things can really get

precarious. While a fake-out breakdown could be at work, this kind of weakness

so early in a year that is supposed to be mildly fruitful is a bad sign in my

book. Let's take a look at EBAY as it could contain a big warning for us:

I will be

watching EBAY very closely from here as it should be an excellent canary in the

coalmine. I cannot even imagine the NASDAQ being strong with a stock like EBAY

cratering. And I cannot imagine the rest of the market staying healthy with a

cratering NASDAQ.

The madness

continues, so be careful out there!